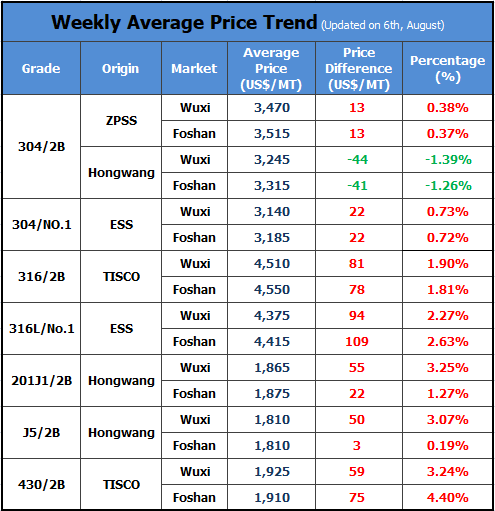

Trend||SS304 slumps by almost US$150/MT.

Last week, both of the stainless steel futures and spots were sold with a bearish market. Until the closing on Friday (6th, Aug), Contrast 2109 dropped by US$153/MT. Also in Wuxi market, the cold-rolled SS304 by private-owned mills decreased by US$141/MT, and the 4-foot mill-edge price went down to US$3,140/MT.

According to the stainless steel statistics, last week, in Wuxi sample warehouse (warehouse receipt registered in Shanghai Futures Exchange is excluded ), the total inventory decreased by 10,400 tons, down to 409,400 tons.

304: The fears of policy changes relieved. Prices might get back to increasing.

In the context of production limit and power rationing policy, all jurisdictions start to execute the plan gradually. Many mills have received notice stated that the production volume shall not surpass the total volume of last year. Plus the shortage of raw materials, the production of 300 series has been greatly affected. In July, the production of 300 series is 1,569,000 tons, 68,400 tons less than last month, and the decreasing percentage is 4.18%. In August, the policies will still be the most influential factors to the production volume, but the pressure on the supply side will be reduced.

Last week, the new resources arrived less, and thereby the inventory volume of 300 series is being consumed. The inventory of 300 series decreased by 7,000 tons. Although the logistics is recovering, the arrival is not large as before. And the continuous typhoon also makes an obstacle during delivery.

From the perspective of demand, due to the previous high prices, the downstream buyers hesitated in purchasing. As soon as the prices decreased to their approval range, the sales in the market regain their activeness. On Friday, when the stock prices warmed up, people kept buying, so the inventory pressure is little and traders tended to raise the prices.

What is uncertain?

1. Last week, mills wanted to send out the new resources quickly before a new approaching typhoon. It is predicted that the new resource volume will be enlarged. If demand cannot keep up with the sudden larger supply, it is possible that traders might choose to reduce the price to collect their capital. If the actual reduction of the production limit policy is not large as predicted, the prices will drop.

2. If the actual reduction about the production limit policy is not large as predicted, the prices will drop.

200 series: The inventory maintains low, which is a boost in price.

Last week, based on the inventory data of Wuxi market, 200 series was 43,100 tons which are 800 tons lower. In July, production limit, environmental protection, storms, and typhoons cause production to decrease in most of the steel mills. Supply to market dropped, and the inventory has been consuming in July.

Based on current productivity, the production volume of some mills reduced significantly because of environmental maintenance and power rationing policy. Thus, the supply for 200 series has been decreasing. The profit of cols-rolled SS201 recovered, to about US$60-US$78/MT, which is still not ideal as 300 and 400 series. Overall, under the raw material shortage, low productivity and low inventory, the prices of 200 series will maintain at a high level.

400 series: The price of high chrome fell, stopping 400 series prices to increase.

After the latest purchasing price of high chrome by mainstream steel mills was released, the EXW quotation of high chrome gets closer to the bidding price. Last week, the price was reduced to US$1,688/50 base tons, US$125/50 base tons lower than before. Because of the decrease in price, the price of 430/2B is hard to maintain the increasing force. For now, the guidance price of 430/2B of TISCO is around US$1,925/MT and JISCO is US$5/MT lower. Other mainstream quoting prices are about US$1,925/MT.

However, the electric power control is still happening in Inner Mongolia, Hunan, Guizhou, Guangxi and Xichuan, so the supply of high chrome is low in July and August, making the price of high carbon ferrochrome difficult to keep falling.

Last week, the inventory of 400 series keeps reducing, to 80,600 tons which is 2,600 tons lower. In August, the production volume of 400 series is predicted to decrease and the supply will tighten up.

Summary:

304: Thanks to the decrease in both stainless steel futures and spots, the risk is degraded. But because of production limit and power rationing, the price will probably increase in the future. It is predicted that the cold-rolled 304 by private-owned mills will rise by US$47/MT.

201: The price will increase by about US$31/MT due to the production reduction and low inventory volume.

430: The price of high carbon ferrochrome decreased but has yet to influence the trend of 400 series. The low inventory and less supply will maintain a stable price trend. The price of 430/2B of JISCO and TISCO will stay around US$1,925/MT.

JULY|| Production limit takes effect. Total inventory volume reduced by 90,000 tons.

To stainless steel market, July is robust. SS304 has increased for a month, risen from US$2,790 to US$3,265. 200 series and 400 series also rose by US$234-US$313/MT.

In July 2021, stainless steel enterprises that are above-designated size produced 3,015,000 tons of crude steel, MoM decreased by 90,100 tons and the decreasing percentage is 2.9%; while YoY increased by 17,000 tons and the rising percentage is 0.57%.

All series of production decreased, among which, it is 300 series reduced the most.

The production of 200 series is 923,900 tons, MoM reduced by 18,400 tons and the declining percentage is 1.96%; compared to the same period of last year, it decreased by 71,500 tons, and the declining percentage is 7.18%.

The production of 300 series is 1,569,000 tons, MoM reduced by 68,400 tons and the declining percentage is 4.18%; compared to the same period of last year, it increased by 42,300 tons, and the rising percentage is 2.77%.

The production of 300 series is 522,200 tons, MoM reduced by 3,300 tons and the declining percentage is0.62%; compared to the same period of last year, it increased by 46,200 tons, and the rising percentage is 9.71%.

200 series: Steel mills either reduced or stopped producing, and supply declines.

From the data of July, the total production volume of 200 series slightly decreased. However, to different mills, the production of 200 series fluctuates.

On one hand, Baosteel Desheng swift producing the plain carbon steel to stainless steel. Therefore, the production of 200 series has increased by more than 80,000 tons in July, compared to June.

Officers and soldiers of an Air Force motor transport regiment reinforce the dike along the River (July 23) from Xinhua News

On the other hand, restricted by storms, environmental control and power rationing policy, many mills reduced their production. From July 19th to July 20th, continuous storms hit Henan Province, causing the river to flood over the embankment and spread to the nearby industrial park. Steel mills stopped working for more than ten days. Thereby, the production of 200 series and 300 series were sharply cut. Baosteel produced less 200 series because of electric power rationing. Influenced by the environmental investigation, SDSY also stopped working for at least two weeks, which also makes the 200 series production decline.

Generally, the unexpected reduction in production offsets the increase brought by the swift of Baosteel Desheng, and the total inventory volume keeps declining. But due to the high prices, weak demand, and production recovery of the mills, recently the new resources to the market are getting more, weakening the price-increasing motivation.

300 series: Production volume decreases.

At the end of the second quarter, 300 series remained at high prices. The market mostly predicted the production volume of 300 series would largely increase due to the considerable profit margin. Whereas the news about production limit is approaching in the second half of year. All jurisdictions begin the work to execute the limit for different mills. Not to mention the shortage of raw materials and power rationing, the actual production in July decreases, which is out of many people’s expectations.

Steel mills that reduce more production in the rest of the year are the mills that produced much before, and Ansteel Lianzhong will face great pressure in reducing production. BGXC will be influenced greatly by the power rationing policy.

400 series: Production volume in July is stable, but in August, it will tighten up.

The power rationing policy is still the main reason for the increasingly high price of 400 series. The policy not only restricts the production of high chrome, which is the raw material of 400 series but also limits the running of steel mills. In July, the general production remained.

A steel mill in northwest China cut down the production in June because of maintenance and in July, it has recovered. Other mills, like Ansteel LISCO and TSGT, also had a slight decline.

Besides, it is predicted that in August the flat production of 400 series will reduce by 66,700 tons compared to July’s production volume. A steel mil tells that in August, they plan to cut their production from originally 70,000~80,000 tons/month down to 30,000 tons ~40,000 tons/month. The supply for the 400 series will tighten up in August.

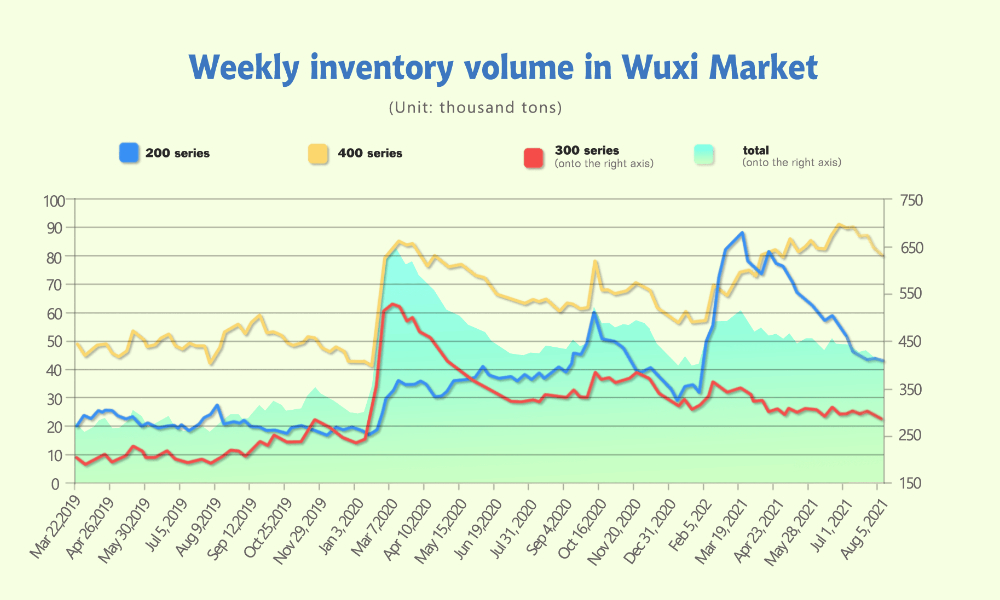

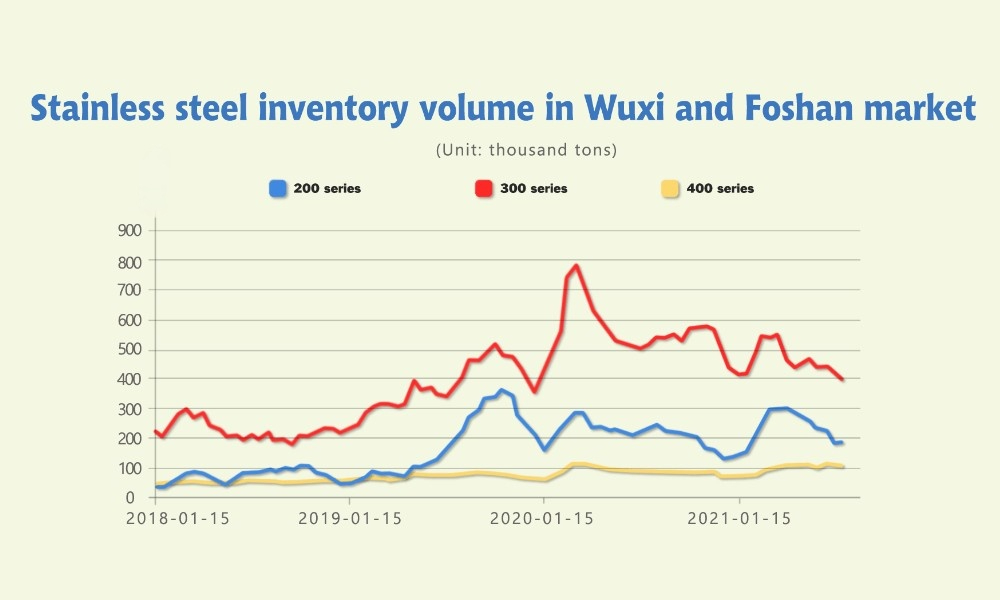

Inventory keeps reducing.

See the above graph, until July, Wuxi and Foshan has consumed 92,600 tons of inventory, and left 685,000 tons. The inventory of 200 series is 183,600 tons, decreasing by 39,300 tons; 300 series is 397,700 tons, decreasing by 44,700 tons; 400 series is 103,700 tons, decreasing by 44,700 tons. People are refusal to the high prices, but the tight supply gradually manifests in the market—— the inventory keeps reducing.

Futures|| As China's demand slowed, iron ore futures prices fell below¥1,000(about US$160).

China’s iron ore futures fell below ¥1,000(US$156)/MT on 5th August, down by more than 5% to its lowest level in recent two months, due to strict domestic steel production control.

The price of the most active iron ore futures for September settlement on the Dalian Commodity Exchange plummeted 5.6% to ¥999(US$154.54) per ton, which is the lowest level since May 27.

Chinese (iron ore) consumption is significantly weakening, and iron ore prices have been fluctuating recently due to different views on the reduction of crude steel production. With the current strict implementation of steel production control, high iron ore prices seem to be unsupported.

The 62% spot iron ore shipped to China was priced at US$185.5 per ton on Wednesday (4th August).

The prices of other steelmaking raw materials on the Dalian Exchange rose, with coking coal and coke futures rising by 2.8% to ¥2,343(US$366) and ¥2,973(US$465) per ton respectively.

*The price of steel bars for October settlement on the Shanghai Futures Exchange rose by 1.0% to ¥5,415(US$846) per ton.

*Hot rolled coil futures prices for automobiles and household appliances rose by 1.1% to ¥5,802(US$907) per ton.

* The September Shanghai stainless steel futures contract fell by 0.9%, to US$3,070/MT.

*China is the world's largest coal producer and consumer. In order to increase supply, China will extend the trial production period of 15 coal mines with a total annual output of 43.5 million tons by another year.

Stainless Steel Market Summary in ChinaStainless Steel Market Summary in ChinaStainless Steel Market Summary in ChinaStainless Steel Market Summary in China