TREND|| Futures of SS304 increases by more than US$180/MT last week.

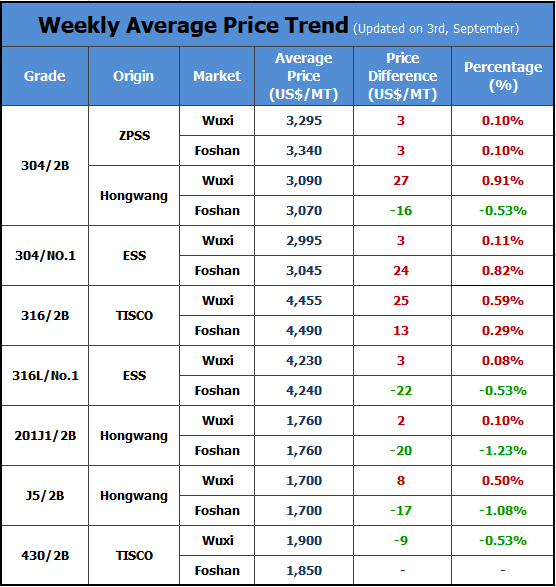

Last week, both the futures and spot markets tended to increase overall. Until the closing on Friday, the stainless steel futures, contract 2110 rose by US$183/MT, hitting US$3,070/MT. In Wuxi market, the price of cold-rolling 304 of private-owned mills increased by US$16/MT last week, and the base price of the 4-foot product lifted up to US$3,040/MT.

304: The production limit policy is still boosting the price.

From the perspective of the raw materials, ferronickel and nickel ore keep rising in price. Recently, steel mills begin to purchase raw materials. Steel mills based in Northern and Southern China bought high nickel-iron at US$227/nickel and a steel mill in Eastern China bought thousand tons of high nickel-iron at US$116/nickel, while other mainstream steel mills remain the purchasing price high.

In the nickel ore market, the production area of nickel ore in The Philippines usually comes to the rainy season at the end of October, when the supply will largely reduce. It is known that many of China’s ferronickel factories have begun stocking up nickel ore to guarantee future production, which temporarily enlarges the demand for nickel ore. What’s more, because epidemic prevention and control remain strict in ports, the working efficiency declines. Not to mention the high cost of sea freight, the purchasing cost rises significantly. In short, the prices of nickel ore and ferronickel will increase.

The production limit never fades away, and even it is stricter in Guangxi Province. Rumor has it that Delong and Guangqing will reduce their output which shortly boosted the futures prices. About the inventory, last week, the inventory of 300 series in Wuxi market reduced by 7,000 tons and decline has lasted for two weeks. According to the market, Tsingshan, Beigang New Materials had their new resources of SS304 launched in the market last week, and totally there were 15,000 tons. What’s more, Delong, JH and other steel mills all have new resources entering the market. However, the agents of the state-owned mills have signed rations to complete every month, so the earlier resources of giant mills consumed much. While last week, the bullish market also encouraged more purchase behaviors, and thereby the demand was strong, accelerating the resources consumption.

Looking broadly, the non-agricultural employment in the US in August grew by 235,000 which is far lower than the presumption 720,000 and it is the lowest increase percentage for 7 months. In the previous global central bank meeting, Fed Chairman Powell stated that it is appropriate to start debt reduction this year, but he hopes to see stronger employment growth. From this point of view, the Fed’s monetary policy will still be biased towards easing in the financial and commodity markets. There will still be good and good effects.

What’s uncertain?

1. The current futures stick market grows better than the spots market. For now, the price of futures is almost at the same level as the spots, but the fast growth will meet a reduction and harm the spots market.

2. Based on the production limit, to earn more profit, some steel mills will sacrifice the production of 200 series to produce 300 series. Therefore, it is probably that the reduction won’t reach that much as the market predicted.

200 series: Production reduces, which will increase the prices in the future.

From the inventory data, until September 2nd, 200 series in Wuxi market slighted fell by 300 tons, lowering to 41,500 tons, which maintains stable.

Last week, the prices of 200 series remained. Until Friday (September 3rd), the base price of cold-rolling 201 J1 in Wuxi market rose by US$16/MT, increasing to US$1,680/MT.

It is known that lately Baosteel Desheng, Tsingshan and Beigang New Materials and other mills will deliver 200 series and the total volumes of cold-rolled products will be about 8,000 tons. Currently, influenced by power control and environmental investigation, steel mills are carrying the production reduction plan. 200 series are reducing the output in most steel mills. In September, it is expected that the production volume of the crude steel of 200 series will fall by 150,000 tons ~170,000 tons. The supply for 200 series will decrease and the prices will tend to increase, and the base price will rise by US$16/MT~us$31/MT.

400 series: The supply for high chrome will rise, whereas stainless steel will be reduced output.

About the raw material market, the power rationing policy keeps taking effect in Inner Mongolia where is the main production area of high chrome. The ratio of power is unstable. The thermal power enterprises are in profit loss, degrading their productivity. In Inner Mongolia, the thermal power output maintains but wind power is expected to increase. In August, the production of high chrome rises much, and it will continue to increase in September.

About the market price, the guidance price of TISCO 430/2B fell to US$1,900/MT, but it was still a bit higher than the market price. As for JISCO, the guidance price was US$1,925/MT. The transaction was not ideal for traders, so the transaction price actually fell, to US$1,850/MT~US$1,885/MT.

The production of 400 series was predicted to reduce in August, and this assumption is extended to September. The supply will be tightened up. Last week, the inventory volume of 400 series dropped by 2,600 tons, leaving 86,200 tons which are regarded as a rather high level.

Summary:

304: Because of the production limit policy, the price of 304 will keep increasing, but it is possible that the fast increase will trigger a sudden drop.

201: The supply is believed to be reduced. The price will tend to increase, rising by US$16/MT~US$31/MT.

430: The transaction was tepid, while the supply for ferrochrome will be enlarged. It is predicted that TISCO and JISCO will cut down the transaction price of 430/2B, lowering to about US$1,850/MT.

NEWS|| Will the anti-dumping policy against Indonesian stainless steel be revoked?

Last Wednesday(September 1st), it was reported that the anti-dumping against Indonesian stainless steel may be withdrawn. Almost instantly, the price of stainless steel stopped increasing, and the closing price of Contract 2110 plummeted to US$2,890/MT, lowering by US$115/MT the next day.

“On July 22, 2019, the Ministry of Commerce issued Announcement No. 31 of 2019, imposing anti-dumping duties on imported stainless steel billets and stainless steel hot-rolled plates/coils originating in the European Union, Japan, South Korea, and Indonesia.”

According to the records of Indonesia's imports, it is mainly divided into three products: cold-rolled (including 2E coils), hot-rolled and semi-manufactured products (mostly are billets). Due to China’s anti-dumping measures against Indonesian hot-rolled plates/coils, hot-rolled imports take the lowest proportion of the three categories. According to customs data, from January to July 2021, the HR stainless steel imported from Indonesia was 150,700 tons, only accounted for 11.8% of Indonesia's total imports.

Still remember the cancellation of the export tax rebate on stainless steel, which is designed to stabilize the supply within China in a way of increasing imports while decreasing export. This time, the rumor of the withdraw of anti-dumping policy is believed to strengthen the aim.

According to customs statistics, China’s stainless steel imports totally reached 1.629 million tons from January to July 2021, YoY increasing by 97.15%. Among, from January to July, the total amount of stainless steel imported from Indonesia was 1,275,300 tons, 78% of the total stainless steel imports in China. Seeing the below graph, since July of 2020, the proportion of China's imports of stainless steel from Indonesia has continued to maintain a high level. As Tsingshan Indonesia and Delong Indonesia have been put into production, Indonesia has become China's main supplier of stainless steel imports.

Except for ensuring supply in China mentioned above, the reasons why this execution is possible are nickel resources are getting scarce and the prices are extremely high, which also bring burdens for the industry to develop and diversify. Second, it is also connected to the production limit which aims for lowering energy consumption. The HR SS304 output will reduce, and by importing from Indonesia, the supply will increase.

At present, as far as we know, relevant domestic industry stakeholders have not received a review notice from the Ministry of Commerce. Whether the anti-dumping duties will be canceled in the future may be resolved through further negotiations in terms of price commitments.

POLICY|| The production limit falls on steel mill giants and more furnaces will be closed.

Insider said that the hurricane of limited production is finally here!

The National Development and Reform Commission held a meeting on resolutely curbing the blind development of the "two highs" project, and then the super-large steel company BW urgently convened an internal meeting of the group. The intensity of "limiting production" will also be unprecedentedly severe!

As for Baosteel Desheng, the mill has arranged more high furnaces to close; the output will reduce by 50% every month within 2021; the output is reported every day. All arrangements s are executed since September 1st.

A source said that not just the newly-built high furnace cannot be operated, the running high furnaces have to stop. It is real that the reduction will meet 50%!

Because of this adjustment, the steel mill is now working on many negotiations about the cancellations of contracts, including the raw materials due to the sharp decrease in production. Future orders for the fourth quarter are expected to be unavailable. If the customer does not accept the cancellation of the existing order, it may have to be postponed.

That can explain the HR J2 price of futures (October) was opened as high as US$1,725/MT. And it is yet to be sure you can get your products on time.

People believe this might be carried out strictly. They said, “never doubt the governmental enforcement”. The accountability of production cut will be traced office by office, department by department, if the reduction volume does not meet the designated number.

In Guangxi Province, the main production area of high chrome in China, the production cut has carried out earlier. For example, in the steel industry, the production requirement is further reduced. “Companies undertaking the task of reducing crude steel in 2021 will strictly follow the reduction plan to produce less than 80% of the scheduled September production; the short-process steelmaking company's September output shall not exceed 70% of the average monthly output in the first half of this year. "

Due to the electric power rationing, a stainless steel enterprise suffers production loss.

September 3, 2021, due to the impact of power cuts, a large-scale stainless steel finishing enterprise in South China will suspend production for 2 weeks, 7,000-8,000 tons of finishing products will be influenced. Meanwhile, since its cold-rolled 400 series factory is in the same area, the output of its 400 series cold-rolled products will also be affected.

FUTURES|| Fluctuating price trend. The futures once spiked over US$150/MT.

Last week, people in the stainless steel industry experienced a strange time. The price trend changed every day. One day it went up, then it returned down. The process repeatedly came up, making the situation more mysterious.

- September 1st

- September 2nd

- September 3rd

Affected by this two news, stainless steel futures spiked.

- September 4th

At 1:30 pm, the futures stock market opened and blew up. Contract SS2110 once increased by more than US$155/MT, hitting US$3,080/MT.

At 3 pm, stainless steel futures contract 2110 closed at US$3,070/MT, increasing by US$163/MT, holding 53,069 positions which were 9,675 positions higher, and the transaction volume reached 163,114 positions.

About the sharp rise, some people believe it is related to the production limit policy and the energy consumption issue. However, others could not agree for the reason that the suspension of high furnaces does not influence the production of 304. They believe that the increase results from the news of Indonesian imports.

A high furnace in China

Anyways, after Tsingshan’s futures spiked in the afternoon, the mill has stopped accepting orders. People guessed that if Tsingshan deliberately made up an increasing trend.

Stainless Steel Market Summary in ChinaStainless Steel Market Summary in ChinaStainless Steel Market Summary in ChinaStainless Steel Market Summary in ChinaStainless Steel Market Summary in China