TREND||304 drops by US$96/MT, stainless steel prices tend to fluctuate.

Last week, both stainless steel futures and spot market trends moved upward. Until last Friday (August 27th), Stainless steel futures contract 2110 increased to US$2,865/MT, which rose by US$16/MT within one week. As for the spot product, cold-rolled 304 of private-owned mills in Wuxi market, the price of 4-foot product increased by US$62/MT, reaching US$3,000/MT. Will the rising trend last?

304: Nickel price is increasing. 304 price will probably increase.

Steel mill giants began to purchase ferrochrome for September, giving a bidding price that was largely reduced by US$124/50 base tons. However, high nickel iron maintains the price high. Lately, a steel mill in Eastern China made a purchase deal of nickel at US$223/nickel, which is US$3/nickel higher than the former mainstream transaction price. Because the import flow from Indonesia to China is less than expected, the ferronickel supply in China is tight still.

Therefore, the price of nickel ore kept increasing last week. Until August 27th, the quotation (CIF) 1.5 nickel ore of The Philippines was US$87/MT, which was US$3 higher. At the end of October, the production area of nickel ore in The Philippines will enter the rainy season, which will significantly affect the output of nickel ore. Currently, many factories producing ferronickel in China have prepared for the stock of nickel ore to guarantee future productivity. And thereby, the demand for nickel ore bursts out. Besides, recently, the sea freight has kept increasing these days so does the production cost of nickel ore, making the ore price maintain high. In all, both the prices of ferronickel and nickel ore are predicted to rise.

In the market of scrap metal, because of the pandemic and the expansive price, the scrap metal from the downstream enterprises reduces, whereas steel mills have great demand for it. Last week, a steel mill giant in southern China increased the prices of 304 scrap metal two times, totally increased by US$78/MT and it seems to remain the increasing trend shortly.

From the perspective of inventory, last week, 300 series declined by 2,300 tons, lowering to 299,700 tons, which draws a period on the increasing mode. Under the production limit, Beigang New Materials, LISCO and other steel mills have plans for production reduction. It is predicted that the inventory is of little possibility to be stocked up.

Currently, in Shanghai Futures Exchange, the registered warehouse receipts are only 15,900 tons which are 27,000 less than the mid-July. Until the closing of Friday, the price difference between contract 2109 and contract 2110 widened to US$86/MT. According to the market news, the settlement amount of contract 2109 is small which is good for the stock market to boost and carry the spot market up.

What is uncertain in the future?

At the global central bank meeting, FED’s Chairman Powell stated that it is appropriate to start debt reduction this year, but he hopes to see stronger employment growth. It is also emphasized that the reduction of QE(Quantitative Easing) does not directly imply the timing of the interest rate hike. After the debt reduction, the market liquidity is still highly accommodative, which means that the previous market’s expectations for interest rate hikes have failed. In the short term, it is positive. At least, the US dollar index fell last night. And the general rise in the stock market and the bulk commodity market is evidence of this. However, in a long run, monetary policy will stay tightening, and it will hurt commodities in the future.

201: OOS is relieving. The price might fluctuate slightly.

According to the inventory data, until the end of August, the 200 series increased by 7,800 tons compared to mid-August, rising to 199,800 tons in Wuxi and Foshan market.

Lately, the cold-rolled 201 in Wuxi market is expected to have 6,000 tons of arrival; as for the hot-rolled product, the total amount will reach 21,000 tons. Due to the heavy inventory and future arrivals, the prices of hot-rolled products are declining. The 5-foot, hot-rolled stainless steel was reduced by US$78/MT in a week. But cold-rolled products are maintaining. The base price of J1 remained at US$1,650/MT. The price difference between CR and HR is narrowing.

When JH and Beigang New Materials are recovering the production, in a short term, the supply pressure of 201 is high. However, GQ’s plan of production reduction will offset the decline. The price of 201 will remain to fluctuate.

400 series: The September bidding price of high chrome falls.

The high chrome price is decreasing. In Inner Mongolia, the power rationing policy is still affecting productivity, but the control is getting loose. In Sichuan, the power rationing policy is also taking effect, but for now, the policy is effective on only 3 small furnaces, which influences little on the high chrome supply. Influenced by the latest ferrochrome bidding price by Tsingshan, the quotation of the ferrochrome prices mostly declined, by US%78/MT, decreased to US$1,571/MT last week.

About the inventory, in August, the output of 400 series was expected to decline, and so in September, the market supply is tightened. However, the inventory remains high. Last week, the 400 series inventory in Wuxi market slightly rose by 500 tons, increasing to 88,800 tons, and the inventory pressure is rather high.

The price of high chrome declined significantly. TISCO’s purchasing price of high chrome in September is going to release, which will influences the market price to decrease. The steel mills stay firm in high prices, but if the transaction is gloomy, or the traders quote lower than the guidance prices of steel mills, the prices of 430 will remain or go down slightly.

Summary:

The main contract of stainless steel futures once rose to ¥18,000 last week, but affected by the tepid transaction, it fails to maintain the rising force.

The current stainless steel price maintains fluctuating. The price is weak in increasing momentum as well as low in the receptivity of decreasing price. The weak upward momentum comes from the alleviation of tight supply, while the exports and domestic demand are in a downturn in a short term. What’s more, the production limit policy has a small impact on the actual supply of 304. Since the price fell from a high price which was over US$3,250/MT in early August, many people have held a more cautious attitude towards stainless steel prices and future orders. In a short term, the stainless steel cost will restrict the price to fall.

Currently, the high cost of raw materials continuously pushes the prices of ferronickel up, and the ferrochrome prices also maintain high. From the perspective of cost, the profit margin of steel mills is severely reduced. As a result, in a short term, the price is hard to cut down.

The raw material cost won’t decrease lately. Considering that the production volume of 300 series is large, the supply of ferronickel in China is tight, which is beneficial for the raw material prices to increase. Moreover, although scrap metal can be an economical optional choice, it is actually difficult to purchase. The cost is getting higher, which will also raise the stainless steel prices.

RAW MATERIAL|| It is OOS but the price declines.

At every ending of the month, steel mills’ bidding prices of raw materials such as high carbon ferrochrome always is a focus in the industry.

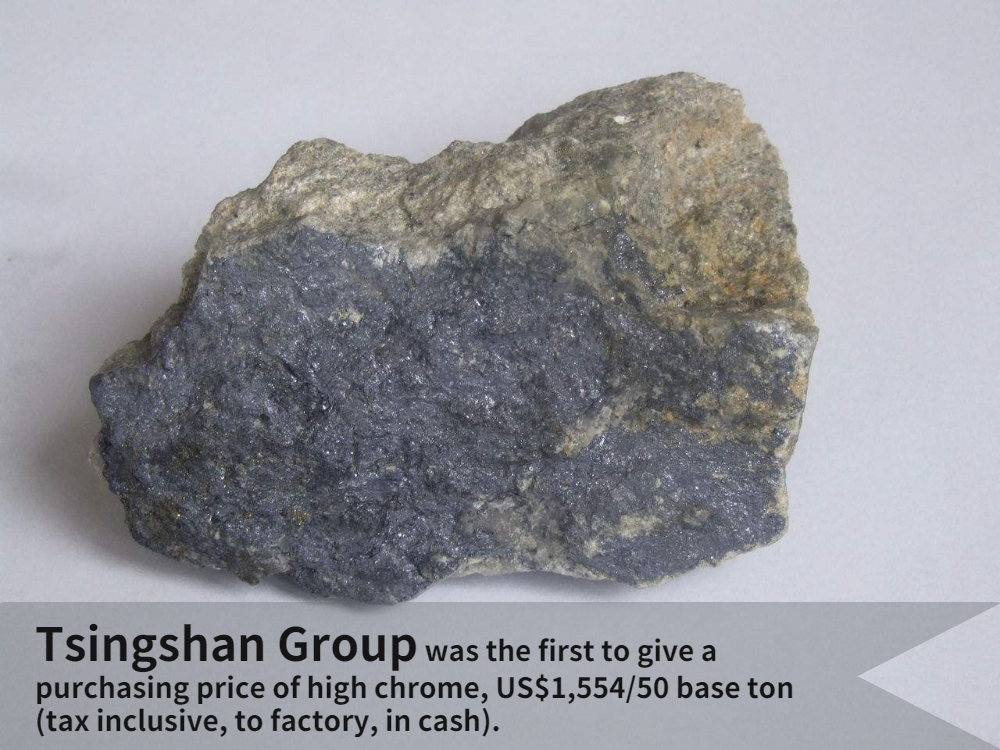

On August 25th, Tsingshan Group was the first to give a purchasing price of high chrome, US$1,554/50 base ton (tax inclusive, to factory, in cash),which is US$124/50 base tons lower than the bidding price of August last month. The price is US$23/50 base tons lower if delivered to Tianjin Port. The delivery time shall not be later than October 10th.

According to the bidding price of TISCO given last month, US$1,648/50 base tons, the bidding price of September might stay around US$1,523/50 base tons.

Last week, the power rationing policy starts to get loose in the high chrome production areas. In Wumeng of Inner Mongolia, the power shortage is reducing.

Last week, Wulanchabu of Inner Mongolia released a notice about the power rationing proportion. Compared to the previous proportion, the shortage of electric power is reduced significantly.

In another main raw material production area, Ebian of Sichuan Province, because of air pollution, the local government required two ferrochrome enterprises to reduce production—— from August 25 to August 31, production is restricted for 5 hours during 14:00 to 19:00 each day, and each company can use one submerged arc furnace only.

Based on the current situation, the influence on high chrome output is smaller in Sichuan.

After steel mills decreased the purchasing price, the quotations of chrome factories were in chaos. Some prices were over US$1,633/50 base tons while others were below US$1,555/50 base tons.

The reason for quotations confusion, the industry said, on the one hand, most factories are currently paying the former orders, and retail spot products are scarce, so the quotations remain high. On the other hand, some other factories producing ferroalloys converted to producing high chromium quoted at a lower price.

In conclusion, the industry generally holds a downward opinion on the price of high chromium in September. The main reason is that the lack of electricity in the main producing areas has gradually recovered. The output of high chromium will increase significantly, while downstream stainless steel companies are reducing production. Chromium price support is weakening with the demand is reducing.

MACRO|| The Fed's TAPERING plan is ready to come out?

The 2021 Jack Hall Global Central Bank Annual Meeting will be held soon. The theme of the meeting will be macroeconomic policies in an unbalanced economy. Fed Chairman Powell will deliver a speech at the meeting.

Market investment sentiment has been cooled off due to the uncertainty about the future expected reduction of the Fed’s balance sheet.

On August 26, the stock markets generally fell. The three major U.S. stock indexes all fell at high levels, and non-ferrous copper and oil all fell from high levels. Nickel and stainless steel futures, which are more concerned in the stainless steel market, also weakened collectively. LME Nickel fell sharply in the afternoon. The closing price fell sharply by nearly $400. Stainless steel futures also followed the trend, the main contract 2110 decreased by US$25/MT, toUS$2,870/MT, and even kept falling on 27th, once hitting US$2,825/MT.

LME nickel

Stainless steel futures contract 2110

Earlier, the US Department of Labor announced that non-agricultural employment increased by 943,000 after the July seasonal adjustment, which is the largest monthly increase since August 2020; the unemployment rate in the United States recorded 5.4% in July, the lowest since April 2020. The data greatly exceeded market expectations. With the improvement of the job market, the Fed’s TAPERING plan is ready to come out, and the market’s concerns about tightening liquidity have gradually increased.

In the Fed’s July meeting announced on August 19, the overall judgment was pessimistic. Most of the members expected to slow down the pace of bond purchases from this year. Most Fed officials believe that "it may be appropriate to start slowing down the pace of asset purchases this year." Some Fed officials also believe that starting the tapering plan in the first quarter of 2022 and increasing the interest rate in the fourth quarter of 2022 is a "logical point in time."

Overall, as the US employment rate improves, the market’s expectations for the Fed’s Tapering plan are getting stronger. The key is whether the Fed will clearly lay out a taper plan, and the other is the Fed's views on the performance of the US economy. Some people believe that the $120 billion monthly debt purchase program should be completely ended in the first quarter of next year. These comments put pressure on the market. However, as the Delta virus brings risks to the economy, the timing of the Fed’s official announcement of taper is likely to be postponed.

Stainless Steel Market Summary in ChinaStainless Steel Market Summary in ChinaStainless Steel Market Summary in ChinaStainless Steel Market Summary in ChinaStainless Steel Market Summary in China